X-trader NEWS

Open your markets potential

The major case of cross-border foreign exchange for 6.5 billion stablecoin in Shanghai exposed regulatory difficulties: Why is it difficult to stop illegal chaos in policy crackdowns?

Author: Shao Shiwei

Why Did "Stablecoins" Suddenly Become "Popular"?

Recently, the concept of "stablecoins" has become really popular. For those who haven't paid attention to Web3 or virtual currencies, "stablecoins" may still be a somewhat unfamiliar term. But as a lawyer who has been deeply involved in blockchain legal services for many years, I come into contact with related businesses and cases every day, and now, it seems to have "broken out of its circle".

However, putting together the following news events in just a few days, it feels somewhat magical.

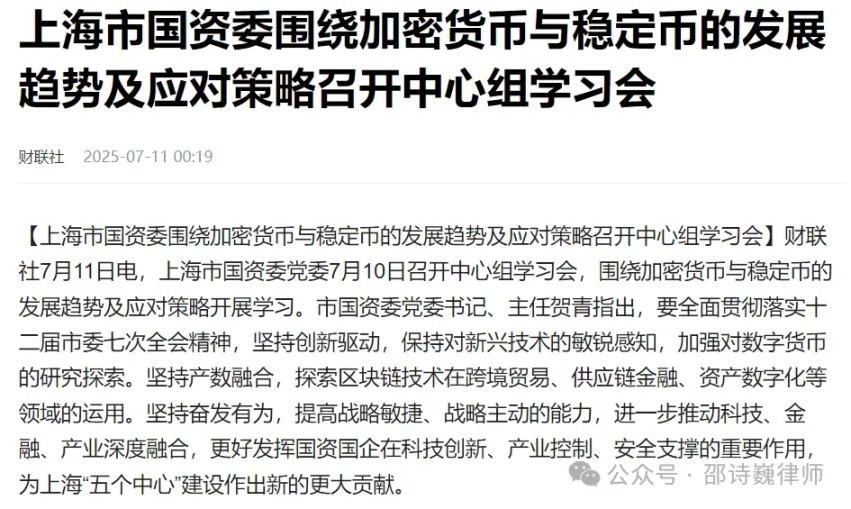

On July 10, 2025, the Party Committee of the Shanghai State-owned Assets Supervision and Administration Commission held a central group study session, focusing on the development trends and response strategies of cryptocurrencies and stablecoins.

Shanghai's 6.5 billion yuan stablecoin cross-border foreign exchange case exposes regulatory dilemmas: Why is it difficult to stop illegal practices despite strict policies?

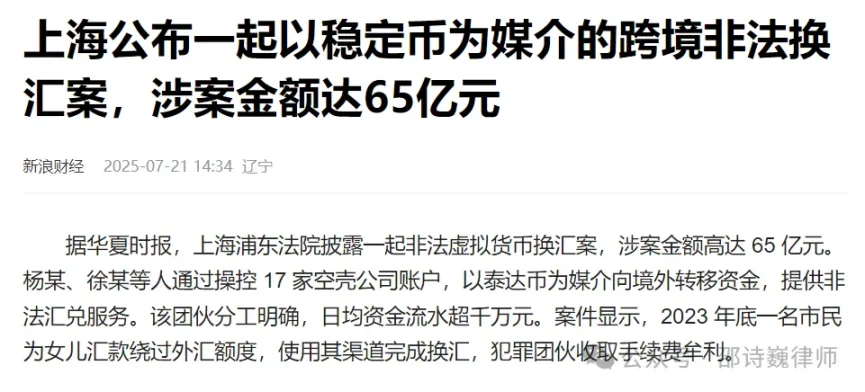

On July 16, 2025, the Shanghai Pudong New Area People's Court announced a major cross-border foreign exchange case using stablecoins as a medium. The case showed that Yang and others, through operating accounts of domestic shell companies, provided stablecoins to unspecified overseas customer accounts, thereby realizing cross-border fund transfers to obtain profits. Over three years, the amount involved in illegal foreign exchange trading reached 6.5 billion yuan.

Shanghai's 6.5 billion yuan stablecoin cross-border foreign exchange case exposes regulatory dilemmas: Why is it difficult to stop illegal practices despite strict policies?

On July 18, 2025, U.S. President Trump officially signed the "Guiding and Establishing American Stablecoin National Innovation Act" (referred to as the "Genius Act") at the White House, marking the first time the United States has formally established a regulatory framework for digital stablecoins.

At the same time, Hong Kong is also about to formally implement the "Stablecoin Regulatory Ordinance" on August 1, 2025, becoming the world's first jurisdiction to establish a comprehensive regulatory system specifically for fiat-backed stablecoins.

Putting these events together, on one hand, major financial centers such as China, the United States, and Hong Kong are promoting the compliance and financialization of stablecoins; on the other hand, some domestic law enforcement agencies still regard stablecoins as a typical scenario of "illegal financial activities".

This dislocation in regulatory rhythms and institutional concepts seems to remind us that it is time to re-examine the realistic role and institutional position of "stablecoins".

Why are black and gray industries so fond of stablecoins?

The core reason why underground banks regard virtual currencies (especially stablecoins represented by USDT) as the first choice for cross-border foreign exchange is that they technically break through multiple bottlenecks faced by traditional foreign exchange, such as quota restrictions, capital pool pressure, arrival time, identity concealment, and differences in jurisdictions. This has directly led to the repeated failure of regulatory policies in the face of "risks of virtual currency anonymity" and "risks of virtual currency money laundering".

First is the issue of "quota restrictions". According to China's personal annual foreign exchange purchase quota system, each person can purchase a maximum of 50,000 US dollars per year. Traditional underground banks often rely on splitting identities and forging trade documents to avoid this restriction. However, after the emergence of stablecoins, chain transfers through encrypted assets such as USDT or BTC can completely bypass this quota ceiling, enabling one-time cross-border transfers of millions of US dollars.

Second is the issue of "capital pool pressure". In the past, underground banks needed to prepare foreign exchange positions both domestically and abroad, which was high-risk and costly. Stablecoins, however, have broken the logic of bilateral provision. It only requires collecting RMB domestically to instantly complete currency-to-currency or currency-to-fiat conversions on overseas exchanges, reducing the start-up threshold from tens of millions to several hundred thousand yuan.

Third is the issue of "arrival time". Traditional bank wire transfers usually take T+1 to T+3 working days and must submit a series of compliance materials. In contrast, on-chain transfers can be completed within an average of 10 minutes to 1 hour, operating 24/7 without holiday restrictions, which greatly improves the efficiency of capital flow. This also makes customers generally willing to pay 1% to 3% or even higher fees for "express arrival".

Fourth is the issue of "identity concealment". Traditional cross-border remittances often leave a relatively complete regulatory chain through bank flows, customs declarations, etc. In virtual currency transactions, however, with the help of on-chain address mixers, desensitized wallets, and overseas exchanges, the connection between fund flows and real identities is fragmented through multiple layers, significantly increasing the difficulty of investigation by law enforcement agencies and prolonging the case-solving cycle.

Finally, there is a regulatory arbitrage point frequently exploited by gray industries: differences in jurisdictions. Traditional foreign exchange requires dealing with regulations in both domestic and foreign jurisdictions, but with stablecoins as a cross-border medium, illegal funds often complete the final fiat conversion in jurisdictions with loose regulations. Even if domestic accounts are frozen, overseas funds can still be safely withdrawn, thus achieving free movement across "different regulatory regions".

It can be said that the intervention of stablecoin technology has not only reconstructed the operation mode of illegal foreign exchange but also greatly enhanced the efficiency and concealment of black and gray industries. This low-threshold, decentralized, and strong cross-border tool is becoming a new technical infrastructure for "gray flows" of cross-border funds.

Why does the country continue to crack down heavily on virtual currency-related crimes?

China's severe crackdown on virtual currency-related crimes is based on the following two core regulatory logics:

First, virtual currencies have natural anonymity and cross-border liquidity, which are difficult to be effectively penetrated by the traditional financial regulatory system and are easily used to conceal and transfer illegal gains.

The "Interpretation of the Supreme People's Court and the Supreme People's Procuratorate on Several Issues Concerning the Application of Law in Handling Money Laundering Criminal Cases" implemented on August 20, 2024, has officially listed "trading through virtual assets" as one of the money laundering methods. This means that judicial organs' crackdown on "virtual asset money laundering" has entered a clear and institutionalized stage.

Second, as a country with strict foreign exchange controls, the borderless nature of virtual currencies can easily become a technical tool to evade regulation and realize illegal foreign exchange.

Such behaviors not only disrupt financial order but also pose a substantial impact on macro-control and national economic security, mainly including:

Statistical distortion: Since the virtual currency transaction chain is not controlled by local regulatory agencies, the actual outflow of foreign exchange cannot be accurately included in official statistics, resulting in "data black holes" in international payments and foreign exchange reserves;

Macro-control failure: The central bank cannot accurately grasp the real situation of market supply and demand for foreign exchange, which may lead to misjudgment of the timing of exchange rate and interest rate adjustments, affecting policy effectiveness, and even requiring the use of a large amount of real reserves to "fill" the outflow gap;

Tax and asset loss: Illegal foreign exchange through virtual currencies to avoid taxes leads to the loss of deposit reserves, cross-border tax sources, and anti-money laundering data in the foreign exchange settlement and sale links.

Since the "September 4th Announcement" in 2017 first clearly defined virtual currency-related businesses as illegal financial activities, regulatory efforts have been continuously increased. The "card-breaking" special campaign starting in 2020, while cracking down on traditional bank card crimes, also prompted underground banks, online gambling gangs, etc., to gradually switch their fund channels to digital asset tools such as stablecoins. Even though the "September 24th Notice" in September 2021 reaffirmed that virtual currency-related businesses are illegal financial activities, in reality, due to the high liquidity, low threshold, and strong concealment of stablecoins, their use has become increasingly active in gray industries.

It is against this background that a group of intermediaries engaged in "buy low, sell high" arbitrage, commonly known as "U merchants", have emerged. They do not directly participate in currency circle projects nor are involved in upstream links such as money laundering and gambling, but they are often accused of high-risk charges such as illegal business operations, helping information network criminal activities, and concealing criminal proceeds due to providing matchmaking transactions and earning exchange differences. They are also a "high-risk marginal group" involved in criminal procedures in current judicial practice.

Can stablecoins really be "eliminated" by continuous policy crackdowns?

From the "September 4th Announcement" in 2017 to the "September 24th Notice" in 2021, and then to the continuous severe crackdowns on virtual currency transactions and illegal foreign exchange activities across the country since 2023, the density and intensity of regulatory policies have significantly increased. However, as a lawyer who has handled a large number of criminal cases in the fields of virtual currency, illegal operations, and illegal foreign exchange, and can be said to be a "witness" in the handling of each criminal case, I have been constantly thinking during the handling of each criminal case:

Can this way of continuous severe crackdowns really achieve the goal of effectively combating crimes and punishing illegal and criminal activities?

This doubt arises because in many of the cases I have接触 or handled, there are many such situations:

Those arrested are all "marginal figures":

Whether it is the virtual currency trading platform cases I have handled, or underground banks, foreign exchange companies, and money laundering networks, a very common phenomenon is that those arrested are often ordinary employees who work for wages, "drivers" who help move money, intermediaries who introduce foreign exchange and receive a small amount of introduction fees, and U merchants who earn differences by buying low and selling high. Of course, there are also corrupt officials involved in such cases. But these people are often neither decision-makers nor core members of the chain, let alone the real beneficiaries.

The principal offenders are at large, and law enforcement means are difficult to pursue:

The operators and big bosses of many cases have long fled abroad, and some have even changed their nationalities. Transnational law enforcement has costs. Even, my clients have repeatedly mentioned to the handlers that the principal offenders are in Hong Kong, China, but the case-handling units have not taken the initiative to arrest them because the mainland police have no law enforcement power in Hong Kong.

National losses are difficult to recover, and high investment in judicial resources yields limited returns:

Take the cross-border online gambling case with 400 billion yuan in involved flows cracked by the Jingmen police in Hubei in 2022, which is known as the country's first virtual currency case sentenced by the court.

From filing to judgment, it took nearly two years and invested a lot of manpower and material resources. Although the court finally made a confiscation judgment on "partially frozen virtual currencies", according to insiders, the actual recovered amount was far lower than expected.

The reason is that a large number of involved assets are stored in foreign trading platforms or overseas company accounts in the form of virtual currencies. For example, Tether, the issuer of USDT, is registered in the United States. Chinese law enforcement agencies face many practical difficulties in hoping for its cooperation in judicial seizure.

The fragmented law enforcement reality only treats the symptoms but not the root cause

The above problems reveal a reality: for the real perpetrators, the cost of breaking the law is often just letting "marginal figures" serve their sentences; while for those arrested, they are just a link in the entire chain - neither organizers nor planners, nor have the ability to bear the consequences of the entire chain. Although the criminal law has a deterrent effect, in practice, "introducers", "transporters", and "exchangers" have become the main targets of punishment, which treats the symptoms but not the root cause.

At the same time, it is worth pondering whether the large amount of police and law enforcement resources invested by the country in each case can换来 systematic governance effects. Let's review the typical cases officially reported in recent years:

Shanghai Pudong Court announced a 6.5 billion yuan stablecoin cross-border illegal foreign exchange case, in which Yang used 17 shell companies to manipulate cross-border "knock-for-knock" (2025)

Beijing police cracked a 2 billion yuan virtual currency serial case, using USDT for "cross-border knock-for-knock" to provide RMB-foreign currency exchange channels for gamblers, cross-border e-commerce, etc. (2024)

Qingdao police in Shandong and the Qingdao Branch of the State Administration of Foreign Exchange jointly cracked a major underground bank case with an involved amount of 15.8 billion yuan (2023)

Jingmen police in Hubei cracked the country's first virtual currency case, a cross-border online gambling case with 400 billion yuan in involved flows (2023)

Hangzhou court in Zhejiang sentenced Zhao and others for illegal business operations by collecting dirhams in Dubai, purchasing USDT, and selling them domestically for RMB in a circular arbitrage, with an involved flow of more than 43.85 million yuan (2022)

Shanghai Baoshan Court sentenced Guo Zhaozhao, Fan Mopin, and others for setting up websites such as "tw711 platform" and "Huosu platform" for illegal foreign exchange, with an involved flow of 220 million yuan (2022)

In practice, there seems to be a sense of loss of control where "the more you block, the more leaks there are" and "the more you hit, the bigger it gets". The country hopes to achieve a warning effect on the whole society through the punishment of individual cases. However, the actual situation is that everyone is an island, trapped in their own information cocoon. Before the case occurs, these people may not have paid attention to relevant news, or even if they saw it, they did not realize the seriousness of the problem and whether it is related to themselves.

The dominance of stablecoins is something we have voluntarily abandoned

If cracking down on gray industries is "defense", then leading the legal alternative path should have been "offense". But unfortunately, in this field, we have abandoned the initiative ourselves.

Looking back, China was once a global stablecoin power. Today's globally renowned exchanges - Binance, OKX, Gate.io, Huobi, Matcha, etc. - were almost all founded by Chinese people. Once, exchange operation teams were based in China, currency circle information platforms developed in clusters, and most users completed virtual currency transaction settlements with RMB or RMB stablecoins.

But now, all this has become a thing of the past. If it were not for the continuous introduction of policy barriers that forced project parties, platform operators, and investment teams to shut down or choose to go overseas, China would have had a great opportunity to dominate the entire stablecoin ecosystem. What remains in China now are often just the bottom-level workers.

In addition to policy blockades, China has also tried to find another way. Since 2016, the central bank has launched the research and development of digital RMB, clearly proposing the goal of publicly issuing digital currency, with Yao Qian serving as the first director of the Digital Currency Research Institute. Its design goal, to some extent, is to benchmark against US dollar stablecoins and try to achieve the following intentions through digital RMB:

Reduce reliance on US dollar channels, use digital RMB for settlement in cross-border trade, investment, and assistance scenarios, bypass the SWIFT and US dollar clearing systems, and reduce the risk of international sanctions;

Suppress capital flight and illegal foreign exchange by technically replacing the role of USDT, USDC, etc. in the underground financial system;

Provide enterprises and individuals with an "officially produced", compliant, and fee-free digital cash tool to weaken the gray appeal of stablecoins.

However, due to the lack of extensive application scenarios and ecological support for digital RMB, even though the technical level is basically ready, market acceptance remains low. As the saying goes, "you can't make a sweet melon by twisting it hard", and this path has not formed a truly effective payment alternative.

In addition, somewhat darkly humorous, on November 20, 2024, the official announced that Yao Qian had seriously violated disciplines and laws, mentioning that during his tenure, he abused his power to "intimately" support specific technology enterprises and was suspected of using virtual currencies for power-for-money transactions, becoming a key target of those "hunters" who should have been regulated.

The failure of promoting digital RMB to achieve policy goals, on the one hand, proves the limitations of the government path, and on the other hand, highlights another aspect of the "ban" on stablecoins: policy resistance has not eliminated the problem itself, but has only made gray paths more hidden and underground transactions more complex and covert. This has brought more troubles to existing supervision.

What are the advantages of stablecoins? What are their use cases?

On July 18, 2025, U.S. President Trump signed the "Genius Act", officially establishing a regulatory framework for digital stablecoins. In response, Sun Lijian, director of the Financial Research Center of Fudan Development Institute, publicly commented: "US dollar stablecoins are essentially the tokenized projection of the US dollar in the blockchain world and the digital extension of US dollar hegemony. They amplify the global penetration of the US dollar through technical means but also bring new systemic risks. For countries, stablecoins have also become a new battlefield for currency sovereignty games."

Looking back, it seems that what we once regarded as dross is cherished by our opponents and has now become a weapon for them to counter us?

From a technical perspective, stablecoins are programmable digital assets anchored to the value of fiat currencies and operating on blockchain networks. Their core mechanism is to map the book value of fiat currencies into on-chain homogeneous tokens through the custody of off-chain reserve assets (such as USD, RMB, etc.). They can be transferred without relying on bank accounts, are automatically executed by smart contracts, and have the characteristics of high efficiency, decentralization, and low cost.

As such, stablecoins are widely used in the following typical scenarios:

- Cross-border trade settlement: Enterprises can use USD-backed stablecoins such as USDT or USDC to realize second-level cross-border payments, significantly reducing foreign exchange fees and settlement cycles.

- Payment systems in free trade zones and bonded warehouses: Within free trade zones, RMB stablecoins can be used for one-click account allocation, covering various scenarios such as warehousing, customs affairs, and logistics.

- Supply chain finance: Platform enterprises use stablecoins to discount accounts receivable and automatically complete multi-level split payments for upstream and downstream partners.

- Carbon trading and digital asset markets: "On-chain credit assets" with stablecoins as the underlying target can achieve 24/7 automatic matching, enhancing the liquidity of assets such as carbon credits and digital equity.

- B2B and B2C payment tools: As a seamless intermediary in payment scenarios such as cross-border salary payments, study-abroad fee payments, offshore wealth management, and margin management, stablecoins can effectively bridge the "last mile" between traditional financial systems and on-chain economies.

We must recognize that while stablecoins may indeed be used for illegal activities such as money laundering and private foreign exchange trading, they also have tangible positive applications. This is precisely why places like the United States, Hong Kong (China), and Singapore are actively exploring the design of "regulatory sandboxes" for them.

Therefore, when evaluating regulatory policies for stablecoins, we should not only focus on risk labels such as "anonymity" and "borderlessness" but also gain an in-depth understanding of their value in cross-border payments, financial services, and industrial collaboration. Rather than completely excluding them from the system, it is better to face up to their operational logic and consider how to utilize them in a controllable manner.

Stablecoins are not criminal tools; the lack of institutional frameworks is the root of the problem

Stablecoins are not inherently criminal tools but carriers of new financial structures. Whether they are abused depends on whether institutions can keep up in a timely manner. Blind suppression cannot hinder the rapid development of technology. Meanwhile, what we lose is not just the failure to meet regulatory expectations but also the global competitiveness we could have held. (In fact, it seems that we have never actively strived for or taken the initiative to build it.)

From my experience as a criminal lawyer handling cases, the institutional vacuum has led to substantial law enforcement difficulties.

First, the institutional vacuum and the lag in cognition of law enforcement agencies.

Domestic policies blindly suppress and deny the value and significance of virtual currencies, and there is a lack of relevant legal basis and case-handling guidelines. In fact, from a law enforcement perspective, this is not conducive to the smooth handling of cases and the correct implementation of the law.

We represent Web3-related criminal cases in many parts of the country and frequently interact with judicial organs at different levels. It can be said responsibly that the vast majority of grassroots law enforcement personnel still lack basic knowledge of the technical principles and operational mechanisms of blockchain. Our lawyers need to popularize basic concepts to the case handlers first, and then, as the second step, conduct arguments on legal disputes.

For example, in a recent Web3 case we handled, the local judicial authorities hoped that our client would voluntarily hand over hundreds of millions of virtual currencies as "illegal gains". However, in communication with us before the trial, the presiding judge of the case took the initiative to ask us: What do these strings of letters and numbers (addresses, transaction hashes) mean? — The case handlers who decide the fate of the parties know nothing about this field, and this is the norm in many criminal cases involving virtual currencies, Web3 project parties, and exchanges that we handle.

Second, the fragmented crackdown strategy makes law enforcement actions like "whack-a-mole".

At present, China's regulatory path for stablecoins and virtual currencies has not formed a systematic compliance guideline. From the perspective of the prosecution, cases involving virtual currencies and Web3 often lack clear boundaries in characterization, which easily leads to wavering in the application of the law and makes law enforcement personnel run around like "whacking a mole".

Judicial organs have long relied on "plugging loopholes and catching in the act" to maintain the bottom line, which is destined to be a high-cost and low-output approach. As long as there is real market demand and there is still room for cross-border payments and on-chain transactions, "alternative solutions" will always be developed. At this time, arresting "marginal figures" and blocking "downstream channels" is just a continuation of the traditional logic of cracking down on crimes, which is destined to treat the symptoms rather than the root cause and cannot form a truly sustainable governance system.

Truly effective institutional building is neither "purely relying on crackdowns" nor "闭门造车 (building behind closed doors)"; instead, it is to build a system that achieves a dynamic balance between security and efficiency. This is the direction that future financial governance should take.

Conclusion

The real solution is not to block technical tools like "stablecoins" but to build a compliant ecological system that can guide, replace, and regulate them, so that virtual currency regulatory policies can play a precise and effective role. Let those that should be cracked down have nowhere to hide, and let those that should be utilized be used for our benefit.

Disclaimer: The views in this article only represent the author's personal opinions and do not constitute investment advice for this platform. This platform does not guarantee the accuracy, completeness, originality, and timeliness of the article information, nor does it assume any responsibility for any losses caused by the use or reliance on the article information.

Contact: Sarah

Phone: +1 6269975768

Tel: +1 6269975768

Email: xttrader777@gmail.com

Add: 250 Consumers Rd, Toronto, ON M2J 4V6, Canada

+1 6269975768

+1 6269975768 微信

微信 Teams

Teams