X-trader NEWS

Open your markets potential

Galaxy: 2025 Q3 Crypto Venture Capital Report Fund Flow and Trend Analysis

# Cryptocurrency Venture Capital Trends in Q3 2025

Author: Alex Thorn, Head of Research at Galaxy Digital; Translator: @Jinse Finance xz

In the third quarter of 2025, venture capital (VC) activity in the cryptocurrency sector remained sluggish compared to the levels seen during previous bull markets. Although there was a sequential increase from the previous quarter, this growth was mainly driven by a small number of late-stage deals. Valuations have climbed back to bull market levels, while early-stage investment activity has remained active. The macroeconomic environment continues to pose headwinds for fund managers seeking new capital allocation, and recent cryptocurrency market activity in the fourth quarter is likely to further hinder capital deployment in Q4 2025 and Q1 2026. Competition from investment vehicles such as ETFs and digital asset treasury companies has further intensified these challenges.

Despite still being below the levels of the 2021-2022 bull market, VC activity in the sector as a whole remains active and healthy. Areas such as stablecoins, artificial intelligence (AI), blockchain infrastructure, and trading continue to attract deals and capital, with pre-seed investment activity also remaining stable. Given the new government’s commitment to promoting the adoption of Bitcoin, cryptocurrencies, and blockchain technology, the United States’ long-term dominance in this field is likely to be further strengthened.

In Q3 2025, the total venture capital raised by cryptocurrency startups stood at $4.59 billion (a 59% quarter-on-quarter decrease), with the number of deals reaching 414 (a 15% quarter-on-quarter decrease).

Late-stage deals accounted for 56% of the total investment amount, while early-stage deals made up 44%.

Trading-related projects emerged as the most favored segment among VC investors, securing $2.1 billion in funding—including $1 billion raised by Revolut and $500 million by Kraken.

The United States once again maintained its dominance in both funding scale and the number of deals.

In terms of capital raising, investors allocated $3.16 billion to 13 new cryptocurrency-focused VC funds.

## 1. Venture Capital Overview

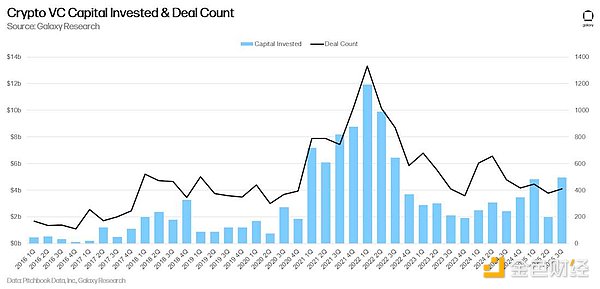

### (1) Number of Deals and Investment Amount

In Q3, VC firms invested a total of $4.65 billion (a 290% quarter-on-quarter increase) in cryptocurrency and blockchain startups and private companies, with the number of deals totaling 415 (a 9% quarter-on-quarter increase).

In the third quarter, a total of seven investments accounted for half of the total venture capital (VC) in the cryptocurrency and blockchain sector: Revolut ($1 billion), Kraken ($500 million), Erebor ($250 million), Treasury ($146 million), Fnality ($135 million), Mesh Connect ($130 million), and ZeroHash ($104 million).

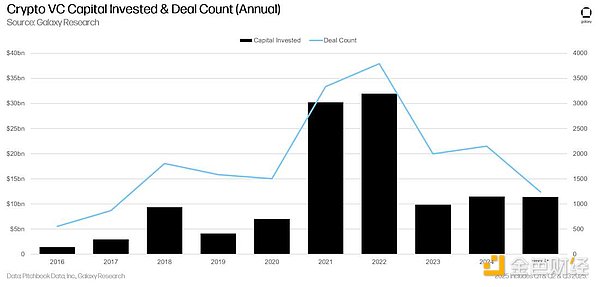

From an annual perspective, although the number of investment deals has not exceeded that of previous years, the total investment amount in the first three quarters of 2025 has already surpassed the same period in 2023 and 2024.

syJJdIro3fPrmztBuj8yFdhdvgRsir1Vzbd8crry.png

## (2) Investment Amount and Bitcoin Price

In past cycles, the capital invested in crypto startups was highly synchronized with the price of Bitcoin. However, this is not the case in the current cycle. Since January 2023, Bitcoin’s price has risen sharply, yet VC activity in the crypto space has failed to keep pace. LPs (limited partners, i.e., capital allocators) have shown weak interest in crypto VC and the broader VC sector; meanwhile, competition from public market instruments such as ETFs and treasury companies has continued to divert capital that might otherwise have flowed to startups.

3Cx5gDSxT0PfoqZjx6e5bpQ0Aw0WkjHrc86oJqZo.png

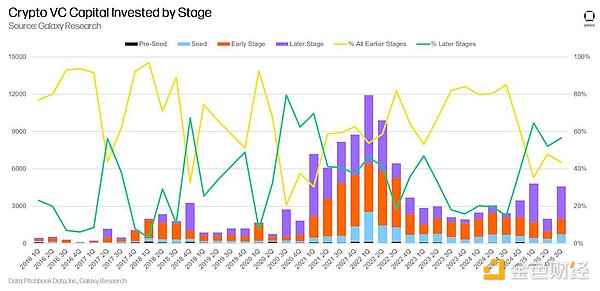

In Q3 2025, 57% of the capital was allocated to mature-stage enterprises, and 43% flowed into growth-stage enterprises.

B611Ceu9TxNKhvon7QYLv619mlcsrvrGoN1JV9Ab.png

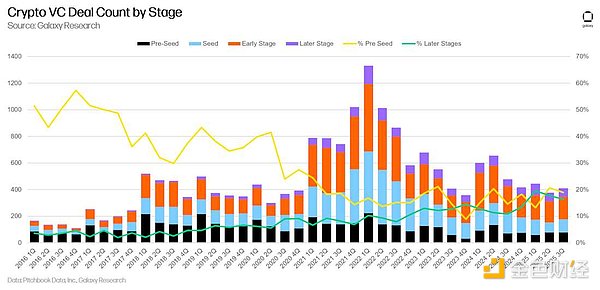

In terms of the number of deals, the proportion of pre-seed deals remained flat quarter-on-quarter and stayed at a healthy level compared to previous cycles. We track the proportion of pre-seed deals to assess the vitality of entrepreneurial activity. Over the past few quarters, the share of late-stage deals has continued to rise, reflecting an increase in the overall maturity of the market.

cGbDfbjS9vEC8ck65jEnWhG0U8q11mf5w0U03Efc.png

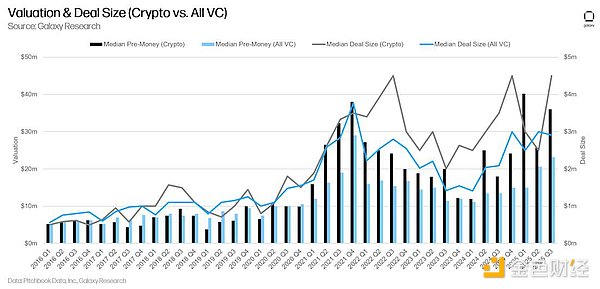

## (3) Valuations and Deal Sizes

In 2025, the valuations of VC-backed crypto companies continued to rise: they exceeded the 2021 high in Q1 and remained close to that level in Q3. Valuations in the broader VC market in 2025 also increased but have not yet reached the 2021 peak. The median deal size in the crypto sector also hit a record high in Q3 2025, with the median single-deal amount reaching $4.5 million and the median pre-money valuation hitting $36 million during the quarter.

# (4) Investment Category Analysis

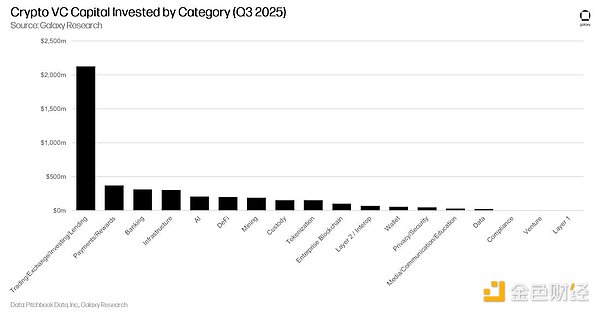

In our classification system, enterprises in the **Trading/Exchanges/Investment/Lending** category raised the highest amount of capital from crypto VC firms, regaining the top spot with over $2 billion in funding—including $1 billion for Revolut and $500 million for Kraken. This segment boasts the most mature business models in the crypto space and has historically accounted for the largest share of VC allocations.

USf4HSUsupLCJ2KvldLlCGUtRGwigs0SrMYebByQ.png

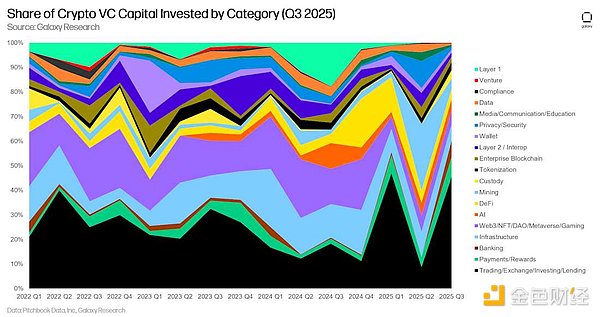

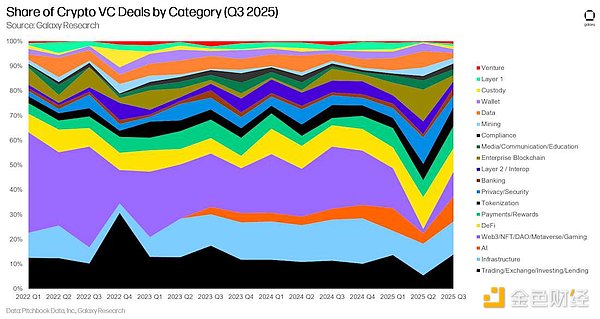

Over the long term, the market share of funding across various tracks reveals interesting trends beyond the persistent dominance of the **Trading/Exchanges/Investment/Lending** category. For instance, the share of the **Web3/NFT/DAO/Metaverse/Gaming** category has declined since its peak during the PFP (Profile Picture) era, while the **Payments/Rewards** and **Banking** categories have shown an upward trajectory.

QygvdjycpumDHoDeGlekAutSrTwsLybUmgXfcdMo.png

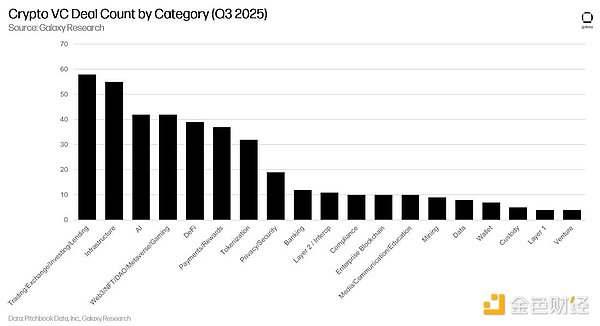

In terms of the number of deals, the **Web3/NFT/DAO/Metaverse/Gaming** category still attracts investment interest, but this interest is now concentrated in earlier stages than in the past (and thus involves smaller capital inflows). Other notable categories include:

- **Infrastructure** (covering companies that provide staking and blockchain access services);

- **Artificial Intelligence (AI)**;

- **Decentralized Finance (DeFi)**;

- **Payments/Rewards** (gaining attention due to the rise of stablecoins);

- **Asset Tokenization** (its prospects are in the spotlight amid shifting regulatory attitudes).

pomXR8O3N6Eg7yqQwXbs4xpM4f8RJooRkAyPk6gz.png

From the perspective of deal count, investments in this sector are becoming more diversified over time.

D5hxV5aNa4gSDHUdv288X6X7h0it7uCK7fk3iaYy.png

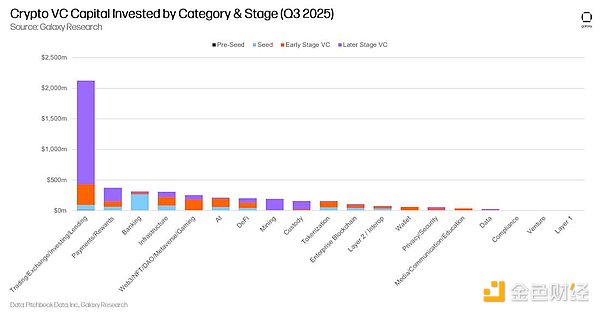

# (5) Investment Stage and Category Analysis

Breaking down investment amounts and deal counts by **category and stage** provides a clearer view of which development stages of enterprises within each category are raising funds. In Q3 2025, the vast majority of capital allocated to the **Trading/Exchanges/Investment/Lending** category flowed to mature-stage enterprises (primarily Revolut and Kraken). By contrast, the main recipients of funding in categories such as **Banking** were growth-stage enterprises.

Faw1V0m8AxQ9PfOg7qTabvezsPquuZ3Zk1awVvWP.png

Analyzing the distribution of investment capital across different stages within each category can reveal the relative maturity of investment opportunities in each segment.

V20xSEdB7Q31UH3hBh07apWCxPsuwxPr6IFeCHdb.png

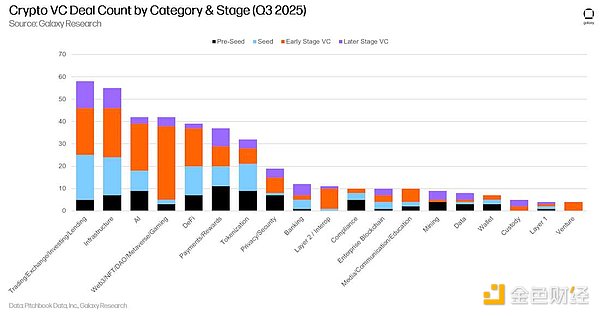

Consistent with previous quarters, the key investment categories in Q3 2025 exhibited a healthy dispersion in terms of deal stages.

wptsU6CreHUxySP17tN13EnyvGpMr1m4vRe0gJc7.png

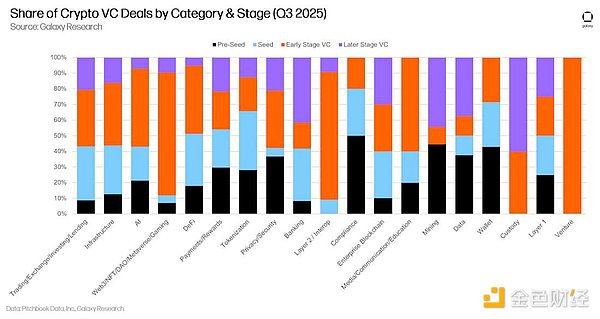

Examining the share of deals at different stages within each category offers insights into the development cycle that each investable category is in.

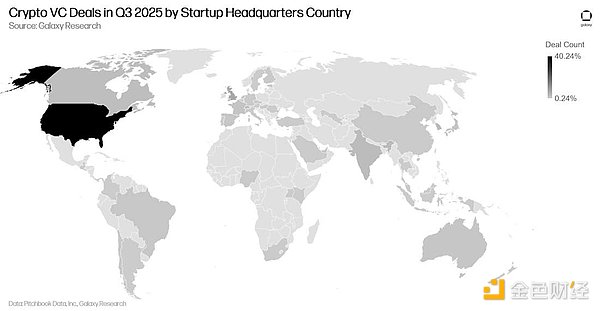

# (6) Geographic Distribution of Investments

In the third quarter of 2025, 47% of investment capital flowed to companies headquartered in the United States. The United Kingdom ranked second with a 28% share, followed by Singapore (3.8%) and the Netherlands (3.3%).

ZCg9gMDyDO4CtJXTvvQdphuZsAfapPMgffb2qW64.png

In terms of the number of deals, the pattern was broadly similar but slightly more dispersed. Companies based in the United States accounted for 40% of total deals, followed by Singapore (7.3%), the United Kingdom (6.8%), and Hong Kong (3.6%).

Y1XMqAa70E5eIsF8txbRq7E82nONTZ7kKqOdDSdJ.png

From the perspective of founding year, companies established in 2018 raised the largest share of capital, while companies founded in 2024 secured the highest number of investment deals.

Y5SdBlpDeRuUfiE5jFQOxyYvtyt9PpiNkPDZbj9E.png

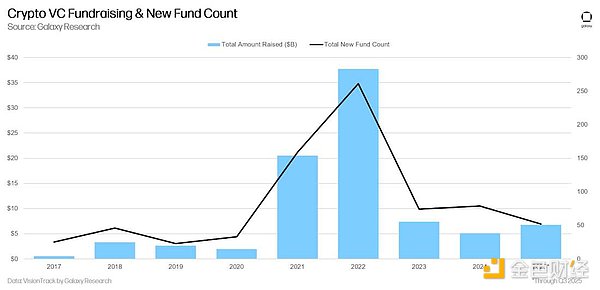

# 2. Fundraising Status of Venture Funds

Although the total fundraising amount increased quarter-on-quarter, the fundraising environment for crypto venture funds remained challenging. The macroeconomic environment and the volatility of the crypto market in 2022–2023 have continued to make some allocators reluctant to maintain the commitment levels they had to crypto venture investments between early 2021 and 2022. Recently, the growing attention on the artificial intelligence (AI) sector has also diverted part of the focus that would have otherwise gone to crypto assets, while spot ETFs and treasury companies are also competing for institutional capital. In the third quarter of 2025, venture funds focused on the crypto sector raised a total of $3.16 billion, involving 16 funds.

V0G8fxxPrZ6r9eQaPVkcaSQbBF0yyr17uXD5PWo9.png

From an annual perspective, the total fundraising amount of venture funds in the first three quarters of 2025 has already exceeded the full-year figure of 2024 and is expected to surpass the 2023 level.

F2xbp7vFfrWlUaGMg6YfN7KD5bJBsqtyvh9PQEBC.png

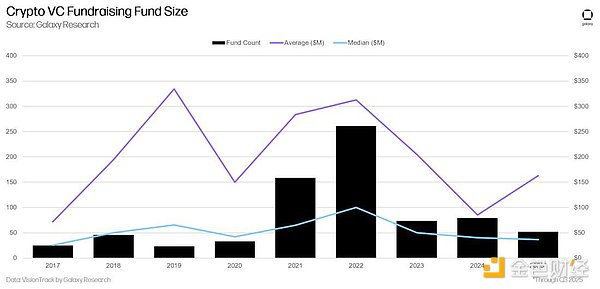

In 2025, the average size of venture funds has risen to $163 million, while the median size has dropped to $36 million.

A3M550QZgjeBp83d1p6AYW30Nm53SIKpOaM8d2rH.png

# 3. Conclusion

Market sentiment is improving and investment activity is increasing, but both remain far below historical highs. In the previous bull market cycles of 2017 and 2021, venture capital activity was highly correlated with the prices of liquid crypto assets. However, over the past two years, despite the rise in crypto prices, investment activity has remained sluggish. This stagnation in venture capital is caused by a variety of factors, such as the declining attractiveness of previously popular crypto venture segments (e.g., gaming, NFTs, and Web3); competition for investment capital from AI startups; and higher interest rates that have generally reduced the enthusiasm of venture capital allocators.

In 2025, mature-stage enterprises led in terms of financing scale. Over the past three quarters, the capital invested in mature enterprises has exceeded that in startups, reflecting the growing maturity of the sector. As the industry as a whole matures, the proportion of pre-seed deals has continued to show a downward trend. With the adoption of crypto technology by established traditional institutions and the fact that a large number of VC-backed companies have achieved product-market fit, the golden age of pre-seed venture investment in the crypto sector has likely passed.

Spot ETPs (Exchange-Traded Products) and Digital Asset Treasury Companies (DATCOs) may be putting pressure on funds and startups. Several high-profile investments by allocators in the U.S. spot Bitcoin ETP space indicate that some large investors (pension funds, endowments, hedge funds, etc.) may be gaining exposure to the sector through these large-scale, liquid instruments rather than turning to early-stage venture investments. Over the past two quarters, attention to spot Ethereum ETPs has increased. If this trend continues, or if ETPs cover other alternative layer-1 blockchains, demand for segments such as DeFi or Web3 may shift to ETPs rather than the venture capital ecosystem. The rise of Digital Asset Treasury Companies (DATCOs) in 2025 may also compete with venture capital for allocators’ interest in the sector.

Fund managers still face a difficult environment. Although allocated capital rose slightly in 2025, the number of new funds has declined for two consecutive quarters and remains near a five-year low. Macroeconomic trends continue to pose headwinds for allocators, but a substantial shift in the regulatory environment may signal a recovery in allocators’ interest in the sector.

The United States continues to dominate the crypto startup ecosystem. Despite the unusually complex and hostile regulatory environment in previous years, companies and projects headquartered in the U.S. have historically completed the majority of deals and received the most investment. This trend has continued this year as the new administration and Congress have begun to pursue the most crypto-friendly agenda in history. We expect the U.S. dominance to strengthen—especially now that the GENIUS Act has been enacted into law. If Congress can pass crypto market structure legislation, it will further attract substantial entry of traditional U.S. financial services companies into the sector.

# Disclaimer

The views expressed in this article are solely those of the author and do not constitute investment advice for this platform. This platform makes no guarantees regarding the accuracy, completeness, originality, or timeliness of the information in the article, nor does it assume any liability for any losses arising from the use or reliance on the information in the article.

Contact: Sarah

Phone: +1 6269975768

Tel: +1 6269975768

Email: xttrader777@gmail.com

Add: 250 Consumers Rd, Toronto, ON M2J 4V6, Canada

+1 6269975768

+1 6269975768 微信

微信 Teams

Teams